China appears to have entered a period of economic slowdown, characterized by weakening growth in both the country’s services and manufacturing sectors. Last month, China's semi-official PMI -- a measure of the health of the manufacturing sector -- was 50.1, signalling that that industry as a whole is dangerously close to contracting. The production sub-index was 52, indicating output barely grew in June. At the same time banks were subjected a surprisingly severe credit crunch, as China’s new government, in office since March, seeks to assert itself economically by tightening the nation’s easy credit environment. Although the credit crunch exacerbated an already worsening economic picture, the national administration and central bank believe it will help foster more sustainable growth.

The slowdown is emblematic of the problems China is facing with its current economic model, which is unbalanced in favour of investment over private consumption, a fact that is finally being reflected in GDP growth. China’s target growth rate for this year is around 7.5%, lower than the actual growth rate experienced each year since 1999. Normally, the annual government target is a low-balled figure, a minimum that should be exceeded. In 2012, for example, the target growth rate was also set at 7.5%, but the actual growth rate ended up being 7.8%. This year, however, it remains unclear whether China will even manage to achieve its target, a possibility that has attracted the world’s concern. While America continues to enjoy moderate overall growth, and Europe struggles on through its own financial woes, China is now downshifting dramatically, having provided years of essential support to world growth following the global financial crisis.

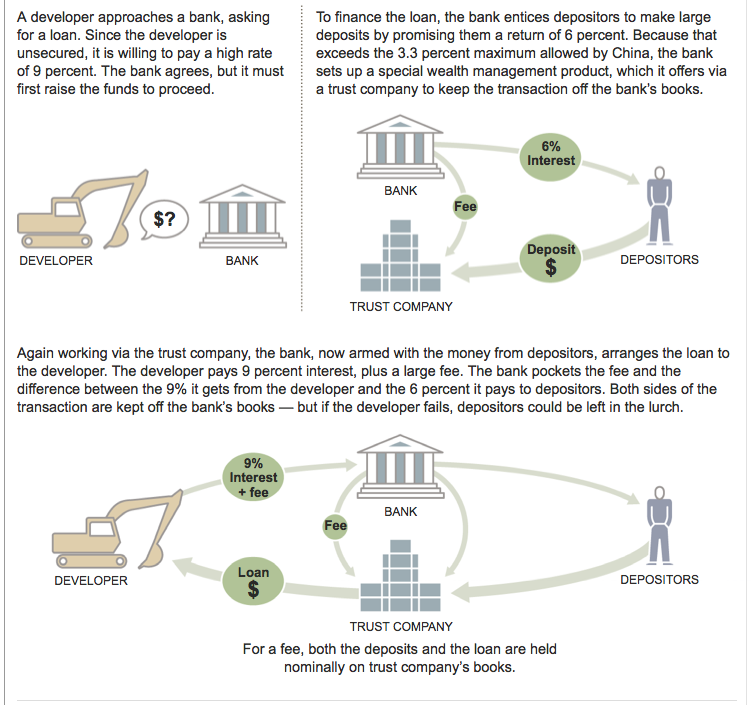

Indeed, the very stimulus programs that allowed China to recover so quickly from the global recession also contributed to a reckless credit environment, inviting the government to intervene. Premier Li Keqiang, second-in-command to President Xi Jinping, and the one in charge of implementing government policy, wants to now teach the banking sector a lesson, so that financial restructuring can produce more sustainable long-term growth. In particular, the government has cracked down on shadow banking, or financial activity that is practiced outside of the regulatory environment, both by established banks and by non-bank financial services companies. Such practices can be beneficial by developing innovative new financial products, but the lack of regulation makes the shadow banking sector a breeding ground for reckless lending.

Source: NYT

China’s leaders are concerned that such risky practices are fomenting systemic risk, and that easy credit may lead to an American-style financial crisis. In the past, such lending has helped the government to match and exceed GDP targets by producing unsustainable goods, in particular excessive real estate. Most alarmingly, an increasing number of loans have gone towards paying off preexisting debts..

The shadow banking crackdown created a credit crunch in mid-June, a time when liquidity was low due to companies paying taxes, and customers withdrawing money in advance of the annual Dragon Boat Festival. It was a startling moment for those who follow China’s economy, as the seven-day repurchase rate for securities –a measure of the cost of lending in the interbank market– shot up to an incredible 25%. In more developed financial systems, such an indicator would be symptomatic of a severe system-wide shock, but in China, where liquidity is injected on a more ad hoc basis, it was more of a wake-up call than a panic alarm. The People’s Bank of China (PBOC) eventually relented, and released some liquidity to bring rates back down and revive interbank lending. But the message from Premier Li and the PBOC to China’s banks was clear: be more cautious about lending, or suffer the consequences.

China’s recent credit crunch is representative of Premier Li’s new conservative direction in financial policy, and for the most part, global investors have reacted with hesitant approval. British bank Barclay’s has hailed what they call the “three pillars of Likonomics:” avoiding stimulus, deleveraging, and structural reform. “We think that economists and policymakers have reached a consensus that China should now tolerate slower growth and focus on structural reforms,” wrote Barclay’s on June 3, estimating that with the necessary reform, China’s economy can continue growing at around 6% to 8% for the next decade.

Others are much more pessimistic about China’s longer-term economic picture. Michael Pettis, a professor of finance at Peking University and a Senior Associate at the Carnegie Endowment for Peace, is a well-known China skeptic. Famously, Pettis has forecast a comparatively abysmal average GDP growth rate of 3% for the country in the next decade, far below the 7% range forecast by the Xi/Li government and Barclay’s.

According to Pettis, China has become addicted to investment, which he believes is subject to the law of diminishing returns: the initial slew of investment drove GDP growth with projects of long-term viability, but over time, maintaining or increasing the same high rate of investment has created fewer and fewer sound proposals, so while nominal growth remains high, in reality, recent years of economic expansion have produced less and less real value for China.

On a real-world level, Pettis cites two major problems with China’s economic model. The first is its state-led western expansion, which relies on government infrastructure projects to lure China’s wealthier easterners into the nation’s central and western provinces. When infrastructure expansion slows, as it inevitably must to correct China’s investment addiction, provinces like Tibet, Guizhou and Shaanxi will see an economic contraction as the easterners find little reason to remain there. The second issue is China’s dramatic environmental degradation, which Pettis believes subtracts about 3.5% from China’s stated annual GDP growth, a figure that fails to take into account the health and economic effects of widespread pollution.

For Pettis, the best prescription for China’s economic ills is to increase household income, thus stimulating the domestic-consumption economy and allowing the investment rate to fall. China’s wages have not increased in line with its productivity over the last 20 years, a problem compounded by the low renminbi, which acts as a tax on imports. By allowing the currency to gain value and workers to earn more money, Pettis believes, China could successfully launch its economy into a new phase without suffering an economic crash.

The Rest of the World

The world’s financial institutions have significantly lowered their GDP growth expectations for China this year, a situation that is looking more and more threatening to slowly recovering America and the struggling E.U.. In this sense, the June credit crunch has been an important wake-up call to policymakers and companies in the West: China’s days of GDP growth over 10%, or even 7.5%, are over.

Whether or not Pettis’ 3% to 4% figure for annual growth is accurate, the fact that China needs to make some potentially painful reforms is indisputable. Premier Li has stressed the overall goal of reducing the state’s role in the Chinese economy, and Chinese policymakers have vowed to take action to boost domestic consumption, moving the country to a more sustainable development path that is less reliant on investment. In most of its reform efforts, the government will have to face down strong vested interests in the Party and in the business world that want to maintain the present environment of easy investment and credit.

If last month’s credit crunch is any indicator, given the choice between suffering the results of a necessary reform, and foregoing reform altogether, the Xi/Li administration seems comfortable with creating a bit of pain and discomfort. The Hu Jintao/Wen Jiabao government of 2002-2012 lacked this boldness, leading some to label those years as a “lost decade of reform.”

China’s new leaders will have to act with both quickly and cautiously as they make up for lost time while balancing the pace of reforms according to the country’s capacity for change. The lesson of the Perestroika-era Soviet Union – that hasty economic and political reform can destroy a nation’s political structure – is an ever-present warning to the Communist Party. But the country cannot afford another decade of hesitancy. And as far as investors are concerned, given the example of last month’s credit crunch, it seems likely that we can expect more economic shocks on the difficult road ahead.